SMM News on July 13, 2025:

The operating rate of China's primary aluminum alloy industry stood at 50.9% in June. After excluding the impact of inconsistent working days from May, it fell by 1.2% MoM, indicating a stronger off-season atmosphere. The PMI for primary aluminum alloy in June was recorded at 36.5%, a significant drop of 5 percentage points MoM from May. It remained below the 50 mark, with a deepening contraction, indicating a notable increase in downward pressure on the industry. The core contradictions lie in weak domestic demand and cost suppression: both the production index (22.9%) and the new orders index (22.9%) hit new lows for the year, reflecting a contraction in domestic demand during the off-season coupled with aluminum prices fluctuating at highs, severely suppressing terminal users' willingness to pick up goods and new orders. Meanwhile, there was a contrast between the high product inventory index (58.8%) and the low purchasing volume index (26.5%), highlighting enterprises' passive inventory buildup, cautious procurement, and the transmission of financial pressure. In terms of exports, the new export orders index (50.0%) remained flat with the 50 mark, but relied on structural support from alternative channels such as Mexico, making it difficult to offset the decline in orders to the US and the expected weakening of overall external demand in the future. Operating rates showed a "stable start followed by a decline" within the month, with orders remaining stable in the first ten days. However, the sustained high aluminum prices and seasonal factors in the middle and late parts of the month led to a slowdown in cargo pick-up. Some enterprises marginally reduced their operating rates due to inventory and financial pressures, and most sample enterprises had planned production cuts for July.

However, as July arrived, it seemed that "plans could not keep up with changes." Although July is traditionally the off-season for aluminum processing, due to the weaker performance of the aluminum billet market compared to primary aluminum alloy, the scale of production cuts by aluminum billet producers has been intensifying. Nevertheless, under the requirement for liquid aluminum alloying and due to the more stable domestic demand for primary aluminum alloy, the surplus liquid aluminum has been redirected towards the production of primary aluminum alloy. SMM expects that the operating rate of domestic primary aluminum alloy producers will likely rebound against the trend in July, but the extent of the rebound may be partially constrained by the high-temperature holidays of enterprises in the next two months.

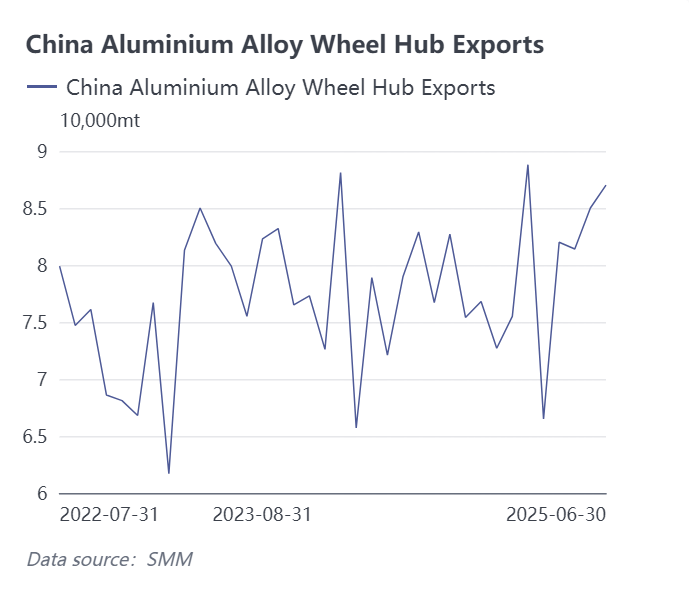

In terms of export data, customs data shows that China exported a total of 85,000 mt of aluminum alloy wheel hubs in May 2025, up 4.4% MoM from April, demonstrating remarkable resilience and up 7.6% YoY. Since the US initiated a tariff war in early April, the aluminum wheel industry, which has directly exported over 30% of its products to the US in recent years, was expected to be "the first to bear the brunt," and market expectations for the aluminum wheel industry's exports were relatively pessimistic. However, the aluminum wheel export data for April appeared "calm," and even more so after the May data was released, exceeding the expectations of most in the market. SMM's aluminum market research indicates the following changes in the distribution of China's aluminum wheel export destinations in May, which warrant market attention:

1. Affected by the tariff hike, the direct export of aluminum wheels to the US in May decreased by 900 mt to 22,300 mt, down 3.9% MoM and slightly down 2.6% YoY. Meanwhile, the proportion of exports to the US fell to 26% in May after dropping below the 30% mark, a rare occurrence in April.

2. After breaking the 10,000 mt mark for the first time this year in April, exports to Mexico continued to increase slightly by 800 mt in May, up 16% YoY, with the proportion continuing to rise to 14%, indicating a significant characteristic of re-export trade.

3. Exports to Morocco have ranked among the top ten for two consecutive months, a cause worth noting. SMM speculates that this is related to some domestic aluminum wheel enterprises establishing overseas factories in Morocco.

From the SMM analytical perspective, after the US tariff hike in April 2025, China's aluminum alloy wheel hub exports demonstrated strong resilience, with the negative impact being smaller than expected. The export rush phenomenon under traditional trade friction warrants attention. Customs data showed overall stable exports in May, primarily due to China's rigid supply chain advantage with 70% of global capacity concentrated domestically, coupled with top-tier enterprises' preemptive overseas capacity deployment in Mexico, Thailand, Morocco and other regions. This strategy not only met overseas new orders but also reduced direct export dependence on the US (current share has significantly declined). The industry's structural adjustment has shown initial results, though continued monitoring is required for overseas capacity ramp-up progress and end-use market premium transmission capability.

Looking ahead, although primary aluminum alloy operating rates may rebound in July, the overall weak stability pattern in H2 2025 for both primary aluminum alloy and wheel hub industries will likely persist, constrained by three ongoing pressures: sluggish off-season demand, unresolved Sino-US tariffs, and high aluminum price negative feedback. Aluminum wheel exports may enter a period of deep adjustment, with substantial recovery awaiting clearer trade policies and effective cost pressure alleviation.